Atlas Insurance, 419 Ta' Xbiex Seafront, Ta' Xbiex.

Insurance cell Sandbox Opportunities in Blockchain Island

Ian-Edward Stafrace, of Atlas PCC, gives insight into how cells can attract innovation.

“Protected cell companies can be seen as platforms to experiment, incubate or launch new technology-driven business models.”

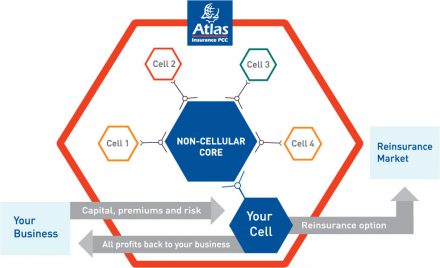

Malta is enabling cells not only for use in self-insurance captives, but also in directly writing third party risks and consumer business. As a full EU member state, Malta enjoys the freedom to provide services and directly cover risks throughout the EEA. It is common for captives and cells in Malta to be profit centres by including customer and ancillary business. Besides added revenue, the diversification enables capital efficiencies.

With more Insurtechs reaching the market, protected cell companies can be seen as platforms to experiment, incubate or launch new technology-driven business models. These are exciting times with the financial services community merging with the tech start-up community to shape the future of this new sector.

Blockchain Island

Malta is quickly becoming a blockchain hub with government strongly promoting the country as “Blockchain Island”, considered to be the world’s first jurisdiction to provide legal certainty to this space. It established a Digital Innovation Authority, which can also provide voluntary certification of such technology, and a regulatory environment for virtual financial assets.

The rapid growth has been palpable at a number of conferences in Malta dedicated to Distributed Ledger Technology (DLT) attracting thousands of delegates and several Fintechs that have set up office on the island.

As Malta is the only full EU member state with cell legislation, and with it quickly becoming recognised as a DLT hub, it is perfectly positioned to enable new innovative technology insurance start-ups or captives to thrive.

Atlas has in fact already assisted Insurtech ventures in micro-testing parametric business models before cell formation that used blockchain smart contracts to automate underwriting and claims processes.

Disintermediation

Billions of euros of capital are flooding into the hundreds of new Insurtech start-ups around Europe and the world. Technology has the potential of transforming the entire insurance value chain including product development, customer acquisition, underwriting and claims management.

Insurtechs can accelerate the disintermediation of traditional distribution channels. While the strategy of large incumbent carriers has tended to include acquisition or investment in such ventures, our experience is that protected cells have helped those with an intermediary or technology background to take over the primary risk carrier role. The desire from some brokers and intermediaries with successful profitable schemes to move from a focus on commissions and fees to a focus on underwriting profits through protected cells has been further boosted by the introduction of the EU Insurance Distribution Directive.

When an organisation realises that it has more data, risk or technology knowledge and ideas than the primary carriers, and it is confident in the potential profitability, it begs the question, why not become the principal and tap into the reinsurance market for support? This is an old idea for captives but one that is dawning on intermediaries, Insurtechs and organisations outside the insurance sector.

With the increasing purchasing power of digital natives, more insurance is being purchased directly online. With full access to the EU single market, cells based in Malta are ideal digital insurers.

Cells targeting consumer business are a growing niche for Atlas PCC with its origins, expertise and risk appetite as an insurer. Atlas traces its almost 100-year history to family businesses representing well-known British and French insurance companies. These merged to form one of the major local insurers in Malta, which later became the first direct insurer to convert to a PCC in the European Union, and the first licensed PCC in Malta.

Incubation

Cells can enable new ideas to be incubated or new business models to be attempted at a far lower cost than a standalone insurer, and without the dependency on a third party principal. This helps organisations that are often wary of indirectly providing intellectual property to insurance principals or fronters in their home country.

In order to spur innovation, Insurtechs often adopt a philosophy to fail fast, fail cheap, and learn continuously. Fitting with this philosophy, should ventures turn out to be unviable in practice, despite different model iterations, these can typically be closed faster in a cell than a standalone company, and the whole enterprise would have come at far lower cost and up front capital commitment.

Breaking barriers

PCCs help break the barrier to entry for new captives or start-up insurers unintentionally created by regulation. A new breed of Regtechs are emerging in time to reduce such burdens, however no solution presents as much promise as protected cells thanks to their capital, cost and governance efficiencies especially in a Solvency II environment.

Well-resourced PCCs can provide cells with the regulatory expertise, infrastructure and economies of scale only usually found in well-developed incumbent insurers. Atlas’ systems of governance allow cells to focus on their specific risks and business plan while providing broader support on regulatory and good governance requirements.

As a single legal entity, Atlas has one board, yet a degree of autonomy is provided to cells through committees that have representatives of the cell owner together with Atlas representatives under the board’s delegated authority. This enables a faster decision making process.

Common key functions including actuarial, risk management, compliance and internal audit apply across the PCC. For Solvency II, such can produce a single Own Risk Solvency Assessment for the entire PCC. The same applies to reporting and disclosure requirements, with one Regulatory Supervisory Report and Solvency Financial Condition Report and all resources in place to meet other quarterly and annual reporting as one single legal entity.

Regulatory sandbox

The Malta Financial Services Authority intends to create a regulatory sandbox regime to help start-ups and established entities alike to have the opportunity to test the commercial and regulatory viability of their technology-enabled innovations. It has issued a consultation document in July 2019 and in which Atlas is actively responding.

Combining this with the flexibility of protected cells could enable regulatory sandboxing to viably apply to insurance carriers rather than just intermediation.

Sandboxes can improve time-to-market and the gaining of real market data. Business plans and projections could then be revised based on experience. Such would also allow a low cost exit in the event tests are unsuccessful.

From our experience of helping prospective cells test their concepts, we know that real market tests can attract investors, venture capital and other funding further enabling scaling up of the business.

Capital

As one of the leading insurers in Malta, Atlas’s core maintains substantial unrestricted surplus funds over Solvency II capital requirements. A cell owner will typically only need to invest own funds equivalent to the cell’s notional solvency capital requirement, which, with small undertakings, often falls far below the typical standalone insurer minimums. At all times, cells retain full protection of their assets, from liabilities of the core or other cells per legislation.

Expertise

Atlas PCC’s team has built expertise in this specialised sector, having assessed and implemented a variety of direct third-party, reinsurance and captive cells. This is also recognised by leading global insurance management companies that use our independent facility for their clients with management outsourced back to them.

Where there are barriers to entry for captives and start-ups including Insurtechs, PCCs like Atlas enable such new entrants into the insurance market promoting innovation.

Bio

Ian-Edward Stafrace is Chief Strategy Officer of Atlas Insurance PCC Ltd having had various roles within the group including commercial underwriting, risk management, compliance and business intelligence. Passionate about innovation, he has further expertise in EU based insurance protected cell structures, from traditional captive models to new consumer InsurTechs using smart contract blockchain technology. To help promote and advance risk management in Malta, he co-founded the Malta Association of Risk Management (MARM) where he is currently a board member.

This article was first published in Captive Review Cell Guide in August 2019.

-

How MGAs can control and build ownership of their insurance…

This article originally appeared on 'The Voice' June 2026 Atlas has just celebrated its first anniversary as an MGAA member. Our application for membership followed hot on the heels of …

Atlas contributed to Captive Insurance Times’ June 2026…

Atlas Insurance PCC has been featured in the June 2026 edition of Captive Insurance Times as part of its Malta Domicile Profile. In the publication, Ian-Edward Starfrace, Chief Strategy Officer …

Captives Move to Centre Stage

This article originally appeared on the Captive Insurance Times: December 2025 issue Captives Move to Centre Stage The captive insurance market in 2025 saw an evolution that significantly outpaced initial …