Atlas Insurance, 419 Ta' Xbiex Seafront, Ta' Xbiex.

Catastrophe bonds, also called cat bonds, are an example of insurance securitization to create risk-linked securities which transfer a specific set of risks (generally catastrophe and natural disaster risks) from an issuer or sponsor to investors. In this way investors take on the risks of a specified catastrophe or event occuring in return for attractive rates of investment. Should a qualifying catastrophe or event occur the investors will lose the principal they invested and the issuer (often insurance or reinsurance companies) will receive that money to cover their losses.

The typical catastrophe bond structure sees a reinsurance special purpose vehicle (RSPV or SPRV) enter into a reinsurance agreement with a sponsor (or counterparty), receiving premiums from the sponsor in exchange for providing the coverage via the issued securities. The RSPV issues the securities to investors and receives principal amounts in return. The principal is then deposited into a collateral account, where they are typically invested in highly rated money market funds.

The investors coupon, or interest payments, are made up of interest the RSPV makes from the collateral and the premiums the sponsor pays. If a qualifying event occurs which meets the trigger conditions to activate a payout, the RSPV will liquidate collateral required to make the payment and reimburse the counterparty according to the terms of the catastrophe bond transaction. If no trigger event occurs then the collateral is liquidated at the end of the cat bond term and investors are repaid.

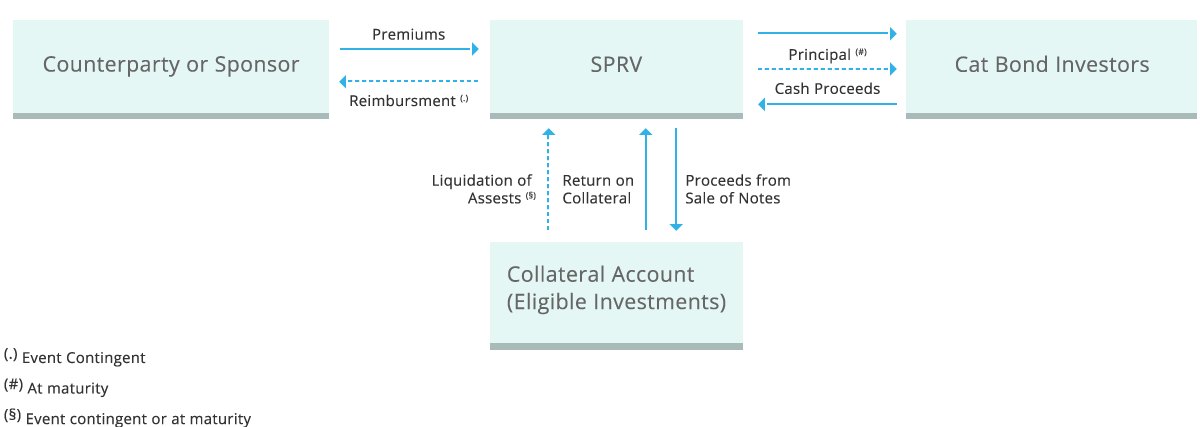

The diagram below shows a typical catastrophe bond structure including where the capital flows from one party to another.

Catastrophe (CAT) Bonds

Catastrophe (CAT) Bonds

Catastrophe bonds, also called cat bonds, are an example of insurance securitization to create risk-linked securities which transfer a specific set of risks (generally catastrophe and natural disaster risks) from an issuer or sponsor to investors. In this way investors take on the risks of a specified catastrophe or event occuring in return for attractive rates of investment. Should a qualifying catastrophe or event occur the investors will lose the principal they invested and the issuer (often insurance or reinsurance companies) will receive that money to cover their losses.

Catastrophe bond structure

The typical catastrophe bond structure sees a reinsurance special purpose vehicle (RSPV or SPRV) enter into a reinsurance agreement with a sponsor (or counterparty), receiving premiums from the sponsor in exchange for providing the coverage via the issued securities. The RSPV issues the securities to investors and receives principal amounts in return. The principal is then deposited into a collateral account, where they are typically invested in highly rated money market funds.

The investors coupon, or interest payments, are made up of interest the RSPV makes from the collateral and the premiums the sponsor pays. If a qualifying event occurs which meets the trigger conditions to activate a payout, the RSPV will liquidate collateral required to make the payment and reimburse the counterparty according to the terms of the catastrophe bond transaction. If no trigger event occurs then the collateral is liquidated at the end of the cat bond term and investors are repaid.

The diagram below shows a typical catastrophe bond structure including where the capital flows from one party to another.